HVAC Organic Demand Trends - August 2024

👋 Hey, Jon here! This week, we are exploring August’s Organic revenue performance. The organic channels in this sample include Google and Bing Organic Listings, Google Business Profile, Organic Facebook, Yelp Organic, and DuckDuckGo.

PS - I am now doing video recaps of these substacks with additional analysis and data on our YouTube channel. If that’s more convenient for you, give us a follow!

Before we get into the August data, I’ll summarize July’s organic performance:

For every $1 spent on Organic in July, $37.10 in closed revenue was generated, and sold revenue increased by 6%, meaning lots of revenue pipeline to start July:

Lead Volume: -0.3%

Average Ticket: +11%

Sold Revenue: +6%

Customer Acquisition Cost: $91.35

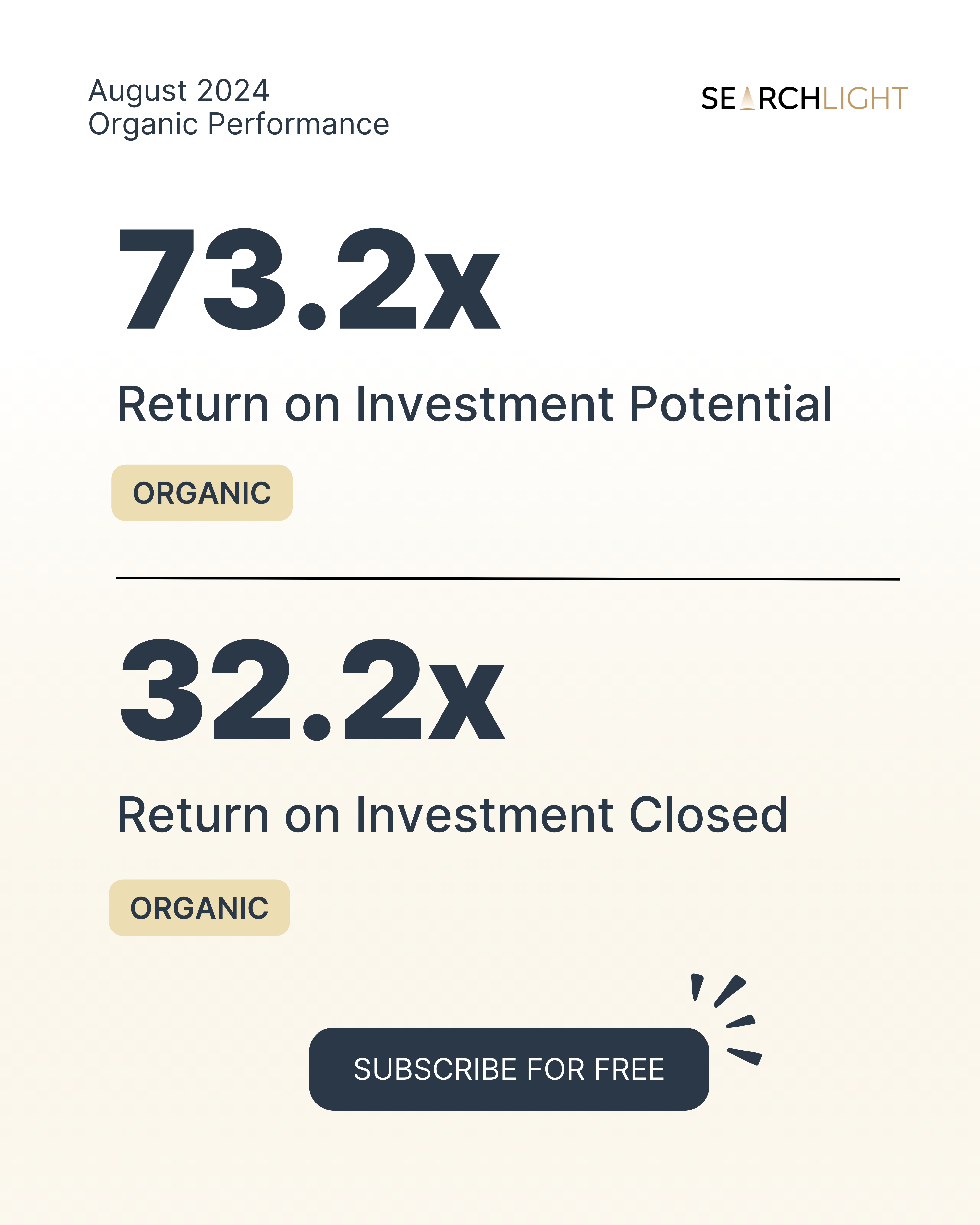

Closed Revenue: +14% (37.1x return on investment)

As usual, shout out to Josh Crouch and his team at Relentless Digital, who partnered with us to measure lead-to-revenue from their organic and LSA management services, enabling us to share these trends with you.

Note that organic spend (based on SEO management fee) decreased by 1.3% month-over-month.

Organic Lead Volume Decreased by 12.6% Month-Over-Month

Lead volume from organic channels in this sample has been on a steady rise since February, peaking in June before slowing down again in July:

+7% from February to March

+1% from March to April

+21% from April to May

+26% from May to June

+0.3% from June to July

This steady progression with two peaks in May and June makes sense, given the summer season, but now that we are off of summer highs, lead volume declined 12.6% in August.

Booked customers (-16%), Matched/Run customers (-14%), and Paying customers (-9%) were also down in August.

This trend is expected with natural demand reductions as we approach the Fall season. However, monitoring and staying proactive with your staff regarding how well your business converts revenue opportunity into sold/closed revenue is critical to weathering reduced top-of-funnel demand.

For example, 48% of the total revenue opportunity in this sample ended the month in the unsold estimate bucket, amounting to millions of dollars.

While our benchmark is to sell / close at least 50% of opportunities (in August, it was 52%), you will likely want to set the bar higher in lower-demand months and make a bigger investment/push in outbound to capitalize on what is already in your pipeline.

The 48% unsold estimates ended up being a higher volume than closed revenue for the month, so while this is well within standard performance, there are still opportunities to improve.

Benchmarks are made to be broken :)

It Cost $97.59 to Acquire a Paying Customer From Organic Channels in August

In August, customer acquisition costs from Organic channels were slightly higher month-over-month and year-over-year.

This doesn’t necessarily mean SEO is more expensive (because it is a “free” channel). Still, when using fees as a cost basis, if demand decreases (fewer paying customers), your costs will increase.

There’s a lot of variability here, and cheaper isn’t always better - it’s always essential to incentivize the right thing with any partners (lower CAC is almost always not the single answer here).

A good metric to pair with CAC when using these benchmarks is closed revenue per brand ($117,000 in this sample for August).

This can help “normalize” the data bit because you may spend much more on SEO and have a higher CAC, but the extra investment generates more volume and vice versa.

Average Tickets Decreased by 8% From The Prior Period

Customers spent 8% less than the prior month but average tickets were slightly higher year-over-year.

Interestingly, average tickets in August were still much higher than in April, May, and June and are the second highest in 2024.

Average tickets tend to be a secondary metric - knowing how much your customers are spending is essential. Still, they can sometimes carry down-trending metrics (e.g. a decrease in paying customers can be ‘hidden’ by a higher average ticket).

Again, it’s important to look at multiple KPIs together to get a sense of the full picture—you don’t want to rely on ever-increasing average tickets if volume is falling.

For example, if you hit your budgeted revenue goal for organic, check the box and call it good, but it was because tickets increased x% and you overlooked falling pipeline or lead volume, it’s possible you can get caught flat-footed the following month if tickets fall.

This is especially important as we head into September, accounting for sold volume trends below.

Sold Revenue from Organic Leads Decreased 13% Month over Month

Sold revenue increased significantly over the last few months:

+65% from April to May

+50% from May to June

+6% from June to July

But much like lead volume, sold revenue decreased 13% from July to August but has increased significantly since March.

Sold revenue helps project next month’s performance—the work needs to be completed and revenue recognized, so in a sense, this is your sales pipeline (some cancellations happen, but they are usually a small percentage).

Knowing that you are starting September with 13% less revenue than in August (as an example), you can make adjustments and prepare your team depending on how your budgeted goals reflect coming off of the peak season.

For example, you may pivot more resources into outbounding, you may focus on service specials to get in the home, focus more on lead handling, speed to lead, etc.

As much as we want to focus on all of these things all the time, the reality is that resources are limited, and sometimes, you can’t do it all at once. Prioritization based on the season, pipeline, and recent data trends can help you focus on the right areas to match your business and market needs and maximize opportunity.

Closed Revenue from Organic Leads Decreased by 17% Month over Month

The closed revenue volume decreased 17% month over month but maintained $32.20 of closed revenue for every $1 spent on organic.

However, total revenue opportunities did decrease 27%, but a higher percentage of those opportunities converted to closed revenue, which meant ROI did not slip as much as it could have.

When looking at closed revenue generated per brand, August was slightly higher than June and only just behind May:

June - August had a strong and consistent showing, but September will likely be more affected by the reduced lead volume, sold revenue, and paying customers.

Until next time . . .

-Jon